Navigating Rural Homeownership In Indiana: Understanding The USDA Loan Map

Navigating Rural Homeownership in Indiana: Understanding the USDA Loan Map

Related Articles: Navigating Rural Homeownership in Indiana: Understanding the USDA Loan Map

Introduction

With enthusiasm, let’s navigate through the intriguing topic related to Navigating Rural Homeownership in Indiana: Understanding the USDA Loan Map. Let’s weave interesting information and offer fresh perspectives to the readers.

Table of Content

Navigating Rural Homeownership in Indiana: Understanding the USDA Loan Map

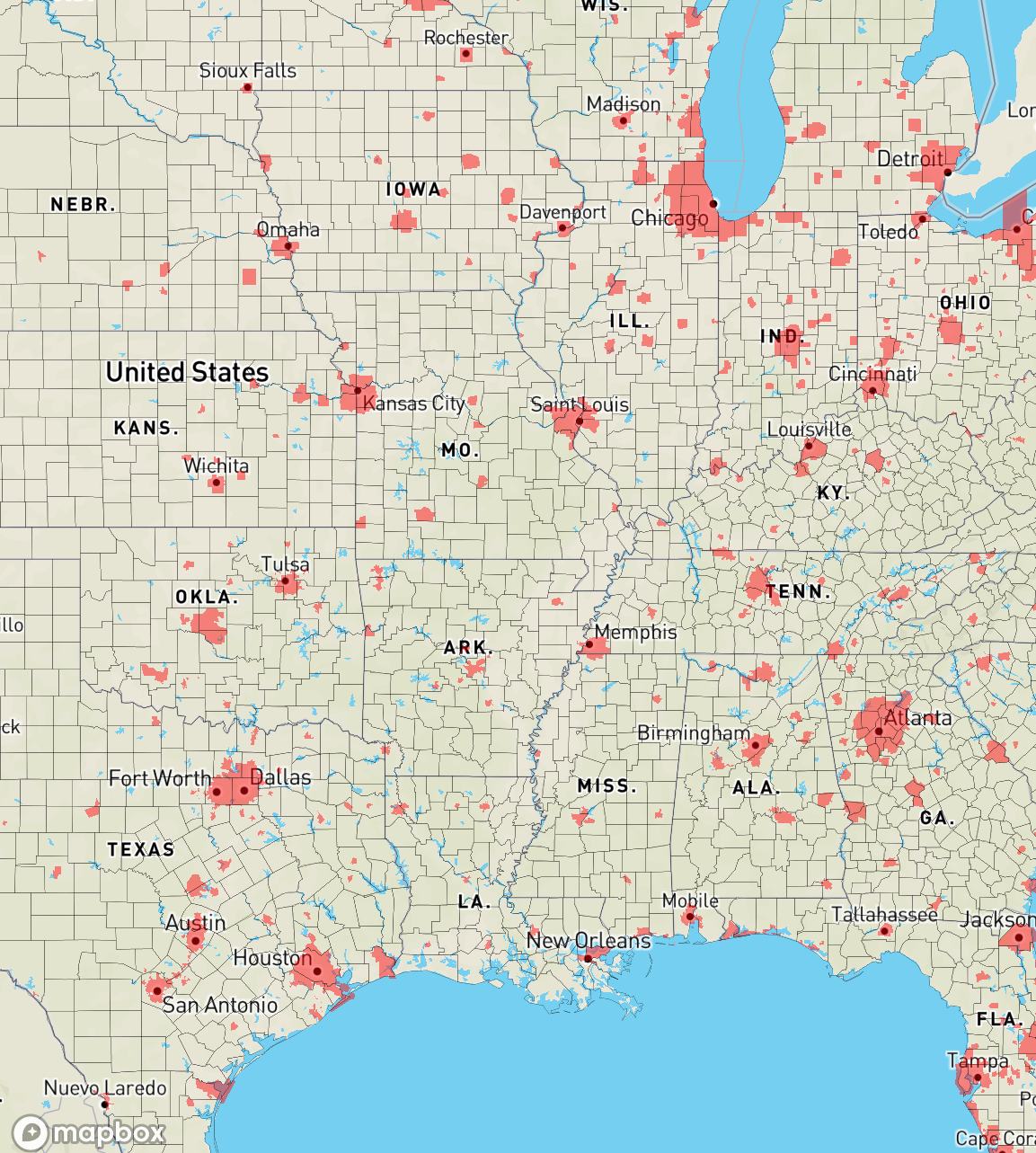

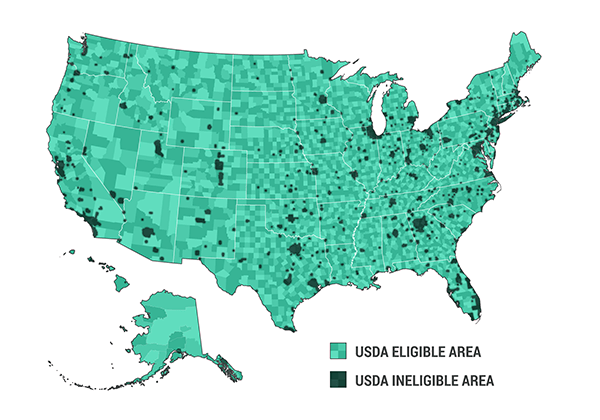

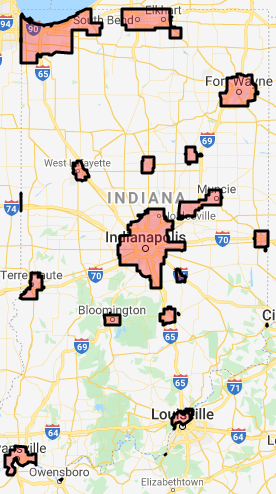

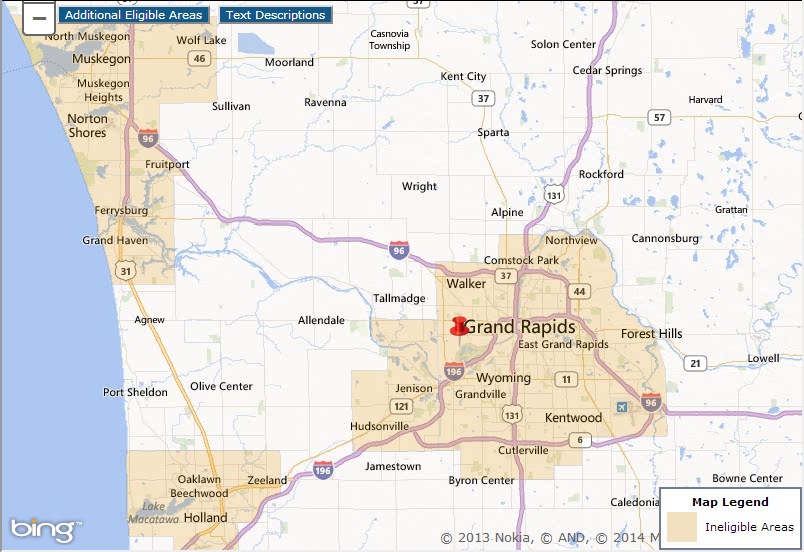

The USDA Rural Development program offers a valuable resource for individuals seeking to purchase a home in rural areas: the USDA Loan Map. This interactive tool provides a visual representation of eligible areas for USDA loans, offering a crucial starting point for potential homebuyers. Understanding the USDA Loan Map and its intricacies is vital for navigating the process of securing a rural home loan.

Understanding the USDA Loan Map’s Purpose and Functionality

The USDA Loan Map is designed to clarify which areas in Indiana qualify for USDA loans, which are specifically designed to promote homeownership in rural communities. The map, accessible through the USDA Rural Development website, visually depicts eligible areas using color-coded regions. These regions are based on specific eligibility criteria, ensuring that loans are targeted towards areas that meet the program’s objectives.

Eligibility Criteria: Defining Rurality

The USDA defines "rural" based on population density, proximity to urban areas, and other factors. To qualify for a USDA loan, a property must be located in an area designated as "rural" by the USDA. This means that the property must meet specific population density requirements and not be located within a designated urban area.

Navigating the Map: Identifying Eligible Areas

The USDA Loan Map is a valuable tool for potential homebuyers seeking to determine if their desired property qualifies for a USDA loan. By entering an address or zip code, users can quickly ascertain whether the property falls within a designated rural area. The map provides visual cues through different color schemes, indicating eligible areas and those that do not qualify.

Beyond the Map: Additional Eligibility Requirements

While the USDA Loan Map serves as a preliminary assessment tool, it is crucial to understand that it only addresses one aspect of loan eligibility. Other requirements include:

- Income Limits: USDA loans have income limits based on the location of the property and the number of people in the household.

- Credit Score: Applicants must meet minimum credit score requirements to qualify for a USDA loan.

- Property Eligibility: The property itself must meet specific standards, including being a single-family dwelling, a manufactured home on a permanent foundation, or a condominium in an approved complex.

Benefits of USDA Loans: Opening Doors to Rural Homeownership

USDA loans offer distinct advantages for eligible borrowers:

- Lower Down Payment: USDA loans typically require a down payment of 0%, making homeownership more accessible to those with limited savings.

- Flexible Credit Requirements: USDA loans are generally more lenient with credit score requirements compared to conventional loans.

- Competitive Interest Rates: USDA loans often offer competitive interest rates, making them an attractive option for borrowers seeking affordable financing.

- Rural Development: By providing financial assistance for homeownership in rural areas, USDA loans contribute to the economic vitality and growth of these communities.

FAQs Regarding USDA Loans in Indiana

1. What are the income limits for USDA loans in Indiana?

Income limits vary based on location and household size. The USDA website provides a tool to determine the income limits for a specific county in Indiana.

2. What is the minimum credit score required for a USDA loan?

The minimum credit score requirement for a USDA loan is typically 640, but lenders may have their own internal guidelines.

3. Can I use a USDA loan to purchase a property for investment purposes?

USDA loans are specifically designed for primary residences and cannot be used for investment properties.

4. What are the closing costs associated with a USDA loan?

Closing costs for USDA loans are generally lower than conventional loans. The USDA website provides a detailed breakdown of potential closing costs.

5. How can I find a lender who offers USDA loans in Indiana?

The USDA website provides a list of lenders who participate in the USDA loan program. You can also contact your local real estate agent or mortgage broker for recommendations.

Tips for Success with USDA Loans

- Consult with a USDA-approved lender early in the process: A lender can provide guidance on eligibility requirements, available loan options, and the overall application process.

- Gather and organize all necessary documentation: This includes income verification, credit reports, and property information.

- Be prepared for a thorough review: The USDA has strict underwriting guidelines, so be prepared for a comprehensive review of your financial situation and the property.

- Utilize available resources: The USDA website provides a wealth of information and resources for potential borrowers, including FAQs, program guidelines, and lender directories.

Conclusion: Embracing the Opportunities of Rural Homeownership

The USDA Loan Map is a powerful tool for individuals seeking to purchase a home in rural Indiana. By understanding the eligibility criteria and the benefits of USDA loans, potential homebuyers can navigate the process confidently and unlock the opportunities of rural homeownership. With its focus on affordability and community development, the USDA loan program continues to play a vital role in shaping the future of rural communities across Indiana.

Closure

Thus, we hope this article has provided valuable insights into Navigating Rural Homeownership in Indiana: Understanding the USDA Loan Map. We appreciate your attention to our article. See you in our next article!